Affiliate Disclosure: Automoblog and its partners may earn a commission if you get an auto loan through the lenders outlined below. These commissions come to us at no additional cost to you. Our research team has carefully vetted dozens of auto lenders. See our Privacy Policy to learn more.

Compare Auto Loan Rates

Compare which options fit your budget, credit score, and term length below.

- All

- 48 to 84 months

- 36 to 72 months

- 24 to 84 months

- All

- 500

- 510

- 550

- 575

- 640

Refinance Loan

Cred Score

Rate Term

APR*

- Average monthly savings of $150

- Work with personal loan concierge to compare options

- A+ BBB Rating

Used Car Loan

Cred Score

Rate Term

APR*

- Great for customers with limited/no credit

- Offers special military rates

- A+ BBB rating

Refinance Loan

Cred Score

Rate Term

APR*

- Customers save 26% monthly on average

- Fast & secure application process

- Sign and upload documents electronically

New Car Loan

Cred Score

Rate Term

APR*

- Below-average credit scores

- Great interest rates

- Smooth and easy online experience

Refinance Loan

Cred Score

Rate Term

APR*

- No application fee

- Lending platform that partners with banks

- Approval and loan terms based on many variables, including education and employment

Since the beginning of the COVID-19 pandemic, the automotive industry has been on a wild ride. Low interest rates, supply chain issues, labor shortages, and high consumer demand have resulted in a highly competitive market and soaring prices for new and used automobiles. But recent developments may bring a change of course for the industry.

In this topsy-turvy environment, potential car buyers may have questions about when the right time to buy is, and whether that time is right now. The answers to those questions are complex, with lots of factors to consider.

In this article, we take a look at what those factors are, how they might affect new and used car prices, and what the experts have to say about whether not now is a good time to buy a car.

The Cost of Automobiles Continues To Rise, but that May Be Slowing Down

As we near the halfway point of 2022, new and used car prices remain at or near all-time highs. But when you look at the details, there are signs that the rate of increase may be slowing down – or even reversing.

New Car Prices Aren’t Rising as Quickly

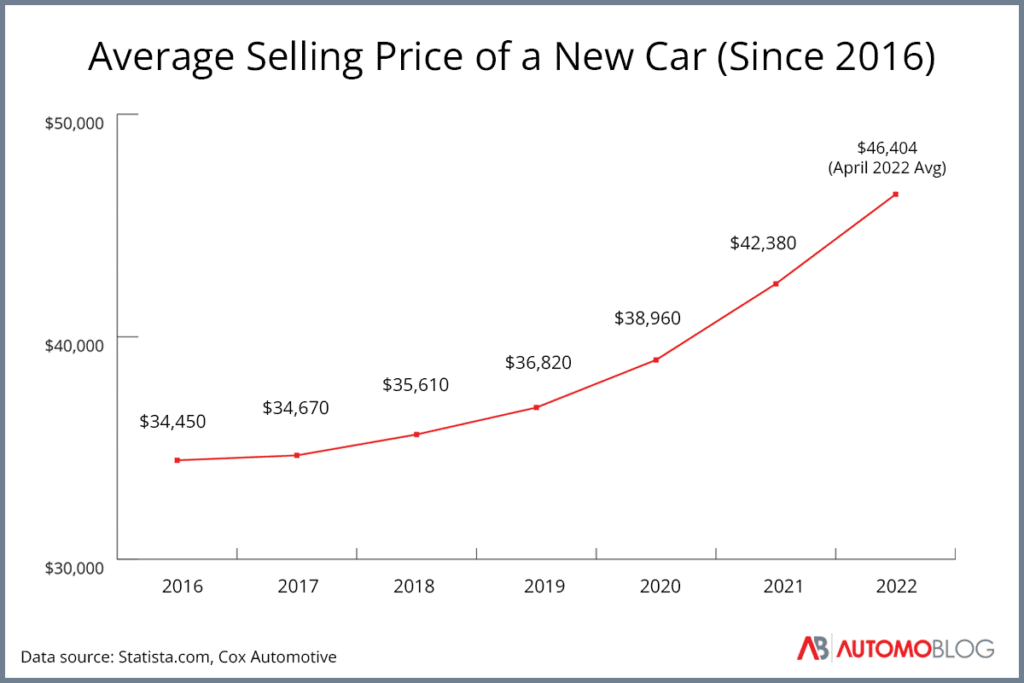

After nearly two years of going up, the average new car price climbed to an all-time high of

$47,243 in December 2021, according to data from Kelley Blue Book. However, in January, that average fell slightly to $46,404. Then, in February, the average fell once again to $46,085. It then fell to $45,927 in March.

Some experts suggest that this recent downward trend in new car prices may continue throughout 2022 and into 2023. But it may be too early to tell just yet. Data from April – a traditionally busy time for dealers when millions of people receive an influx of cash from tax returns – showed the average price rising to $46,526.

If new car prices do drop significantly, dealers could be holding onto stock that would cost more to buy – even at wholesale – than it would later be worth, resulting in negative equity. That could push dealers to slash prices as they look to cut their losses.

The Used Car Market Is a Little More Complicated

Like retail prices for new cars, the average retail price for used cars has shown a downturn followed by a slight increase. While the average price for a used car reached a peak in December 2021 at $28,205 and fell for the next three months, it hit $28,365 in April.

As the decrease continues, it may even be fairly dramatic. At the end of 2021, industry analysts at KPMG suggested that retail prices for used cars could drop as much as 20%–30% between October 2022 and the beginning of 2023.

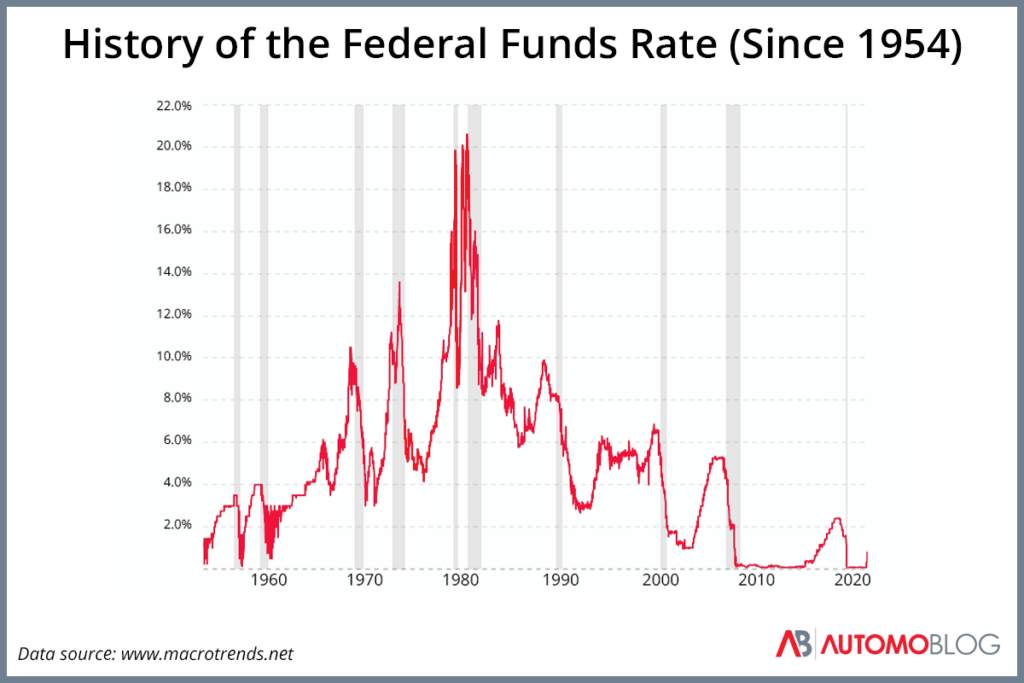

Interest Rates Are Going Up & Should Continue To Do So

After keeping the interest rate near 0% since the start of the pandemic, the Federal Reserve approved an interest rate increase on March 18 and again on May 4 to bring the rate to 0.75%–1%. These were only the first pair in a series of seven interest rate hikes that would take place in 2022 as the government and the Fed attempt to tackle runaway inflation. The potential effect of these increases on the automotive market could be both significant and multifaceted.

On the consumer side, an increase in interest rates means the cost of borrowing money to buy a car will also go up. That increase could negate the drop in sticker prices projected to come in 2022. The result could be a decrease in consumer demand.

But interest rate increases will also affect dealerships that typically need to borrow money to buy stock. According to Reuters, analysts expect that at the end of 2022, the interest rate will likely be two entire percentage points higher than it was at the end of 2021. And while the increase changes the calculations for an individual who wants to buy one car, it’s also a significant change for a dealership that needs to buy dozens of cars at once.

Ongoing & New Supply Chain Issues Could Complicate Things

The continuing microprocessor shortage has been a well-documented issue for the automotive industry. These semiconductors are an essential part of all modern vehicles. Several major automakers have said the semiconductor issue could be resolved this year. But according to Reuters, semiconductor manufacturers and industry experts suggest that it could be 2023 before the shortage ends – a major roadblock for auto manufacturers.

But a shortage of microprocessors is just one of the many supply chain issues that cloud the auto industry. Even industries that produce basic materials are having problems. Dr. Barbara Hoopes, Associate Professor of Business Information Technology at Virginia Tech, points out the complex nature of supply chains in the auto industry.

“An automobile … can contain up to 30,000 parts, each of which may have a unique source, challenges in its industry such as increasing costs, labor shortages, raw material availability, currency fluctuations, and so on,” Hoopes says.

“A disruption in any of those upstream ‘chains’ can cause a disruption in the availability of the final product,” she adds.

Current supply chain issues in the auto industry go as deep as the raw materials themselves. According to the Wall Street Journal, Russia and Ukraine supply nearly two-thirds of the pig iron imported into the U.S. to make steel. The continuing Russian invasion of Ukraine has severely impacted the latter’s ability to mine and export pig iron.

U.S. businesses have looked to other sources of pig iron, such as Brazil and India, to fill the void. But even if companies find a one-to-one replacement solution, further delays would be all but inevitable.

A Sudden Shift to EVs May Disrupt the Industry Even Further

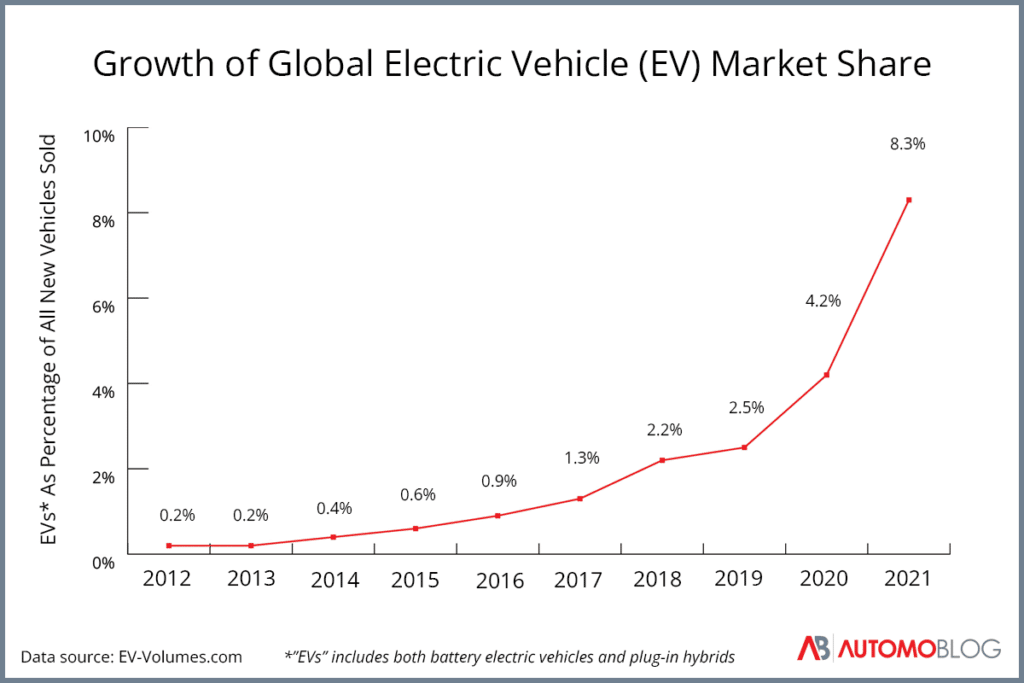

Another issue is the increasingly swift shift in the market away from gasoline-powered vehicles and toward electric vehicles (EVs). Over the last several years, both EV sales and the market share that EVs claim have grown. The rate of that growth has also started to increase.

If this year’s New York International Auto Show is any indication, those trends are likely to continue. EVs dominated this year’s show, with nearly every automaker featuring one, according to autoevolution, signaling a major pivot in the industry.

The growing demand for EVs could be boosted by a proposed increase to the federal EV tax credit. President Joe Biden announced his support for increasing the current tax credit from $7,500 to $12,500. Congress may try to take a vote before this year’s midterm elections.

But Hoopes warns that this shift to EVs may come with more consequences for the automotive supply chain.

“EV car sales are rising and are anticipated to continue rising due to increased fossil fuel costs and concern about the environment,” she says. “EV cars use more semiconductors than typical cars. … This increased demand necessitates new suppliers emerging, or existing suppliers adding capacity – neither of which are inexpensive or quick.”

The Bottom Line: Wait to Buy a New or Used Car if You Can

With all of the variables in play, it’s difficult to predict what will happen with car prices and the auto industry. But what we do know is that, even considering dips earlier in the year, the average price of new cars remains close to its all-time high, and the average price of used cars has reached a new record. Simply put, it’s not the right time to buy a car if you don’t have to.

It’s true that interest rates will continue to rise in 2022 and perhaps into 2023. Higher interest rates would worsen the pain of buying a car at near-peak prices. If you’re concerned about the rising cost of interest, it may be a good idea to start saving for a larger down payment. Putting more money down at purchase will reduce the amount you’ll need to borrow and the amount of interest you’ll be charged.

*Data accurate at time of publication.